I stumbled across a webinar on Automated Market Makers (AMMs) and was surprised to hear Gordan Grant from Genesis mention squeeths as a way to hedge their AMM liquidity provider (LP) positions.1 Genesis is a standard, KYC/AML, TradFi company and so has easy access to liquid option markets on Deribit. The only reason to buy or sell squeeths would be if you want option exposure but are constrained to the blockchain.2 The reason priced-squared contracts are not traded over-the-counter on Wall Street is the same as why there is no peanut butter flavored toothpaste: no one wants it.

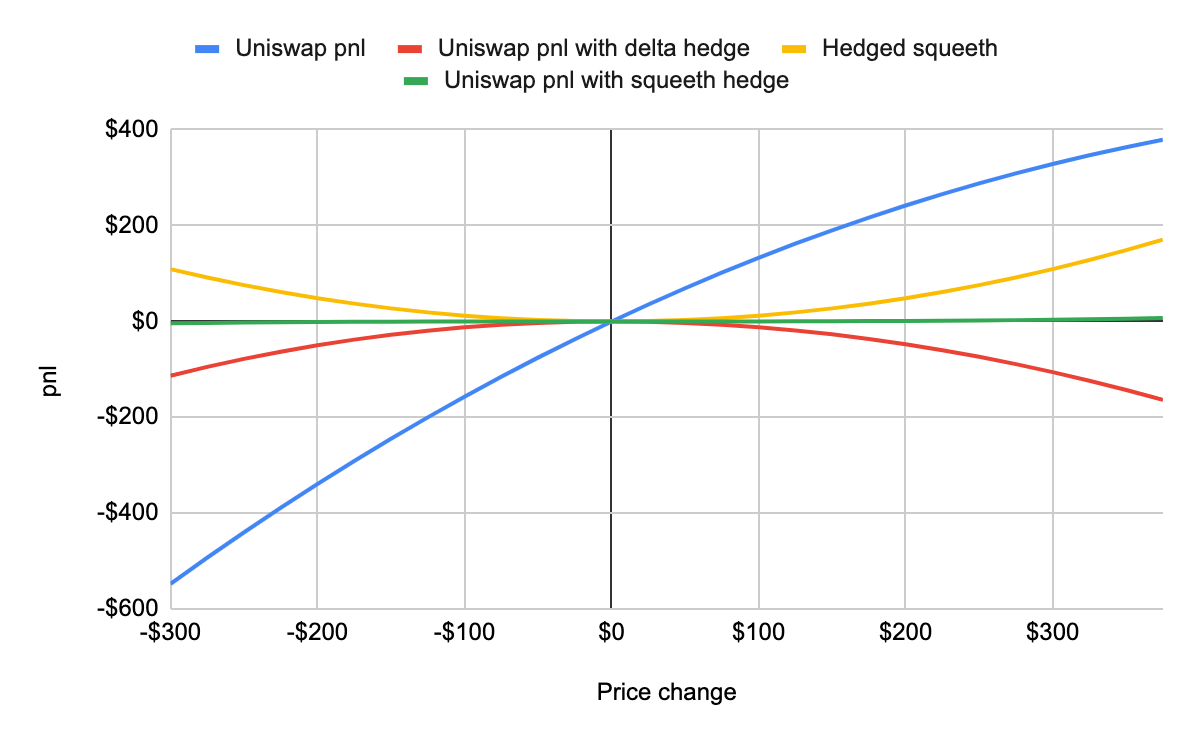

Squeeths are derivatives based on the price of the underlying squared. The best way to see how this product works is via this December 2021 post by Joseph Clarke. The application here is hedging a Uniswap LP position. Below is a chart of the best-case scenario for the squeeth. Here we see the LP’s impermanent loss (IL) as a sad frowning red curve, always below zero. The squeeth is the happy yellow curve that nets the LP’s profit to the flat green line.

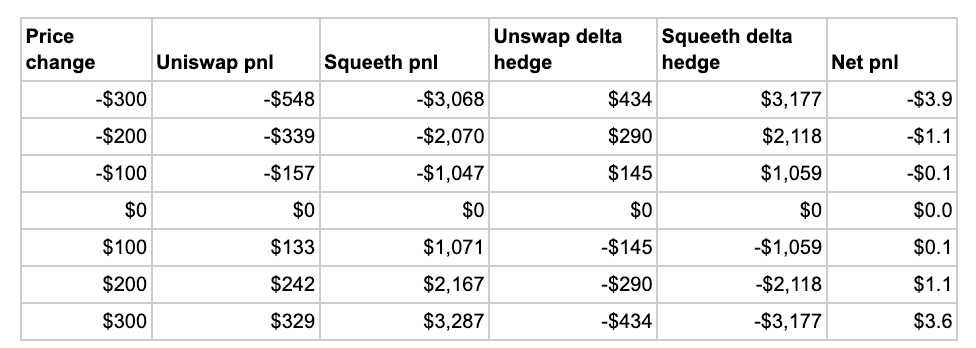

This is also presented in the table below. I have attached a spreadsheet so you can see how these are calculated, and you can compare these formulas to the text, as Clark does a good job of explaining how to derive these values.

Note the squeeth’s value-add to the Uniswap LP is showcased in the right column, which shows a complete immunization of the pnl variability of the naked Uniswap IL in the second column from the left (‘Uniswap pnl’).

The first problem with this application of squeeths is fundamental. If you are making markets (aka providing liquidity) in an option-like product, you should not hedge your book by buying or selling options. Hedging an option with an option is the tactic of a derivatives wholesaler; an options market maker delta-hedges their book.

There are profitable niches for financial product wholesalers, but they generally involve cases where customers are ignorant of market protocols and need costly education. For example, when I worked at KeyBank, a regional bank in Cleveland, we would often take FX or interest rate swap orders from local companies and immediately offload them onto a big investment bank in New York. We would charge a spread for the business, and these are the types of ‘traders’ who brag about making money every day as if they were market wizards. Goldman Sachs does not have the resources to establish relationships with these little companies, so this makes sense.

While it is a valuable job, most of these middlemen don’t even admit to themselves what they do, and who can blame them, given the common sales pitch centered around “eliminating the middleman.” While it might seem obvious to fire these expensive brokers and outsource their services to an Indian customer service team, the customers needing $10MM of Euros in two months would then realize their transaction is much simpler than it appears and shop around. The small bank would either lose the business or have to charge a lower fee. Thus, overpaid regional bank trader/brokers are an equilibrium.

Outside of that general rule, if you bought a squeeth to hedge your LP position, it would not make sense because it implies more delta hedging than if you didn’t buy a squeeth. If you are short gamma, as Uniswap LPs are, your expected cost is the same whether you hedge or not (see my earlier post on that here). However, you should hedge because it will reduce your risk, which will lower your capital requirement. Hedging your delta is a straightforward problem; once you have coded it up, it won’t cut into your time watching the latest cat videos on Tik-Tok.

The squeeth delta at inception is 10.59 in this example, while the LP’s delta is only 1.45. Thus, the amount of delta trading needed to initiate the squeeth will probably be greater than the amount of delta trading needed throughout the life of your LP position. Further, it does not reduce your required dynamic delta hedging, in that as the price moves the squeeth’s delta will change just as the LP position does, in the same direction. This is a large addition to fees.

Another issue is that the additional amount of capital needed to buy the squeeth would almost triple that needed for the Uniswap LP position alone.3 If you add the capital needed for the initial short delta position, you are probably using five times more capital compared to your initial Uniswap LP position.

In the chart presented above, note the LP’s pnl excludes its fee revenue and the squeeth pnl ignores its cost. The happy curves apply to a bizarro world where one is trying to minimize a loss as opposed to maximizing a return. This violates what game theorists call the participation constraint: a sustainable game not only has to assume players will play their best strategy within the game, the best payoff must be greater than zero or they will not play at all. As the squeeth seller requires at least twice as much capital as the squeeth buyer, and the squeeth buyer requires multiple more capital than the LP, the fees charged by the squeeth seller will be more than that of the LP in an efficient market.4 A hedged position that loses money is best avoided.

The only case where a squeeth helps would be cases of ‘jump risk,’ when markets move so quickly that you are not able to delta hedge. These extreme events are costly and rare. Just remember that low probability options, whether bets in sportsbooks, options, or lottery tickets, have the worst expected returns for buyers. These are, literally, lottery tickets, and lotteries make a lot of money for the seller, which is why governments like to monopolize them. The squeeth seller, realizing this, will charge more for the same amount of vega one sees in regular option markets.

Lastly, there’s the bizarre feature where the squeeth’s theta is recalculated every day using the updated implied volatility. They call this method of imputing a time decay a normalization factor. For standard options with explicit maturities, the theta decay shows up in the square root of time term.

In a standard option or variance swap, your initial implied volatility is the cut-off where the buyer makes money if the actual volatility is higher than the implied volatility, and the seller makes money if it is lower. In contrast, the squeeth’s method of resetting the option daily to generate theta means that after the first day, the actual volatility tells you nothing about whether the buyer or seller is making money. This makes a squeeth held longer than a day a position on gamma, but neutral on volatility. Few people have an intuition for this kind of trade, and few would desire it if they understood it.5

If you are an LP thinking about hedging your risk, stick to delta hedging. It’s easy to do, and if you do it twice a day, given the law of Large Numbers, it will hedge your position as well as an explicit option over a couple of months. Squeeths generate a several-fold increase in capital and delta hedging, not to mention the costs implicit in the bid-ask spread of illiquid options, as well as the credit and operational risk lurking in these protocols. It’s a train wreck of a product.

Gordan Grant was humorless but still amusing, calling Centralized Exchanges ‘sexes’ (for CEX) and Centralized Limit Order Books ‘klobs’ (for CLOB). To be consistent he should have called them sexes and slobs, or kexes and klobs.

Opyn sometimes emphasizes their product as SQUEETH, but writing that over and over makes it seem like shouting, so I’m using lower case.

In my spreadsheet, I calculate the squeeth value (price times position) as $23,092.

Given your average LP loses money (see here), perhaps squeeth sellers are under similar delusions, or perhaps doubly so. I have not looked closely at their data, but a market predicated on irrationality is rarely sustainable.

The most common vega-neutral gamma-positive option position is a calendar spread: long the short-dated option and short the long-dated option.

No comments:

Post a Comment