Recent 20% crypto movements have demonstrated again that perp markets continue to gouge their customers. I have written about this several times before, but as it is economically significant, corrupt, and continues unabated, I figured it would be worth revisiting. Alas, reading my old posts, I can see how I muddled my point, perhaps explaining why I am a lone wolf on his issue, so I hope this is clearer.

The funding rate mechanism used to link perp prices with spot prices is a farce in that it does not and cannot tie a synthetic price with a spot price via arbitrage, and in practice, it is used to defraud its users. As a practical matter, the perp price is a Schelling point in that its obvious target is the spot price, and the funding rate is just there to make traders feel comfortable that it is not merely a Schelling point. The fact that there is a vague relation to an equilibrating mechanism is good enough for most traders, as they are happy to use centralized platforms like BitMex and DyDx. As in those cases, many users are happy to have access to perps as long as it seems fair.

One can forgive the perp funding rate scam as its foundational white lie facilitated a much-needed market. In 2016, short or leverage bitcoin was impossible, but there were no exchanges to do this. All one could do was swap one token for another and generate an unleveraged long position. There were no stablecoins or wrapped Bitcoin. BitMex, a centralized unregulated exchange that only took bitcoin deposits, created the first popular perpetual swap, aka ‘perp.’

Instead of an expiration date and settlement in a perp market, a perp anchors its price to the spot via a funding rate mechanism. When the perpetual contract’s price exceeds the spot price, the story is that this implies longer than short demand. The long traders pay short traders a fee proportional to this price premium to equilibrate the market. Crypto funding rates prevent continuing divergence in the price in perp and spot markets.

The perp premium is the percent difference between the perp and spot prices. The spot price could be from external markets like Coinbase, or for centralized perps, from spot markets on their exchange:

PerpPremium = PerpPrice/SpotPrice - 1

The funding rate is like the future expiring once daily, as this premium is applied to 24 hours based on the perp premium. One can apply it to 8-hour windows or anything else, but the standard is to apply the simple premium above and divide it by the number of periods within a day.

For example, suppose you short a BTC perpetual future trading 10% above the underlying index all day. In that case, it’s perp premium—then you will receive a total funding payment of 10% over that day to compensate for the fact that, unlike traditional futures markets, there is no expiry or settlement, as it is perpetual. This sounds reasonable, but to understand why this is not, you must first understand the theory of how funding rates work in swap markets or how basis rates work in futures markets.

The basis in futures markets acts as a funding rate in swap markets, defined as the difference between the futures and spot prices. The chart below shows the horizontal time axis moving from a current futures price to its delivery/expiry date if the black line represents the current spot price.

The basis is the difference between the futures and spot price. It can be positive or negative depending on whether the futures price is above or below the spot price. The funding rate is implicit in the amortization of the basis over time, in that, at expiration, the spot price equals the futures price, so the basis is sure to be zero at that time.

There is no basis for swap markets; a funding rate is applied daily, acting precisely like the basis in futures markets. Swap accounts trade at spot prices, facilitated by broker margin. Here the basis goes from being implicit to explicit.

LongSwapPnL = Notional (p(t+1)/p(t) - 1 - FundingRate)

Funding rates in prime broker swap accounts are charged daily and determined independently of the spot prices, like how a bank sets interest rates. For equity swap accounts common among hedge funds, they are generally a fixed markup to the Fed Funds rate, such as adding 25 basis points when a customer borrows USD to go long and subtracting 25 basis points when a customer goes short (which lends USD to the broker).

Thus far, the similarity of swap funding rates and the futures’ basis to the perp funding rate seems plausible. Two academic articles are generally referenced when presenting perps. The first is by Gehr (1988), which describes how gold was traded at the Chinese Gold and Silver Exchange Society of Hong Kong (CGSE) in the 1980s. This was when trading was not possible around the clock, and there was no internet, so a price had little volatility outside the trading day. The CGSE was unique because its futures market was undated, i.e., perpetual. The market settled daily and held a 30-minute auction to determine the funding rate. Those long gold compare the cost of paying storage and interest on the spot vs. the funding rate; those short gold futures take delivery if they feel the funding rate is too low. This funding rate was added to the spot price to create a new closing price used in the subsequent day’s pnl.

The effect on prices and cash flows in the CGSE futures market was as follows. If the market price closed at 100.00, and the funding rate was determined to be 0.01% over the next day, the cost basis for the next day’s PNL is 100.01. If the price stayed constant at 100.00 each day, the longs would lose 0.01 because the daily pnl would be 100.00 – 100.01 on a long position, where 100.00 is the spot close, and 100.01 is the previous day’s futures close. The traded price would never be 100.01; it would just be used in the daily calculation of the trader’s pnl on the next trading day.

Nobel laureate Robert Shiller (1993) proposed a perpetual futures contract for single-family homes. Unlike a stock index or a commodity, the underlying asset, housing, is challenging to create into a futures commodity because it is not homogeneous like a commodity. Quality varies considerably by location and structure, creating a lemons problem. Shiller proposed a rental index to create a rental return proxy for a housing price index. He proposed a statistical model that correlated with real estate’s average rental return, net of depreciation. This rental return would then be paid by the short to the long.

s(t+1) = f(t+1) - f(t) + d(t+1) – r×f(t)

In the equation above, s is the daily margin change in a trader’s account; f is the perpetual futures price, r is an interest rate adjustment, and d is determined outside the market. While this is interesting, the difficulty in generating a robust rental index for d is probably why this has never been implemented. The market was supposed to trade at a spot price that did not reflect the daily funding charge, d, only its present discounted value. However, rental income, like macroeconomic profit, is challenging to estimate via macroeconomic indicators, and most macroeconomic models work poorly out-of-sample, generating considerable uncertainty for potential traders.

Nonetheless, the estimation method implied that this funding rate would move slowly, like interest rates. There was never the suggestion that the market price reflects the spot price and the funding rate, as there is no spot price in this hypothetical, never-realized market.

The perp premium funding rate charge is like Gehr’s funding rate charge added to the market’s spot price after trading. It is also like the d(t+1) term in Shiller’s model. Thus, at 30k feet, the connection between the perp premium and the funding rate seems consistent. However, the average synthetic/spot price ratio is not determining the funding rate in either of these mechanisms, as it is for perps.

In crypto perps, the modal daily funding rate and perp premium is 0.03%, which annualizes to 11%. This is a significant funding rate compared to interest rates that have been near zero over the period where perps have existed. A 0.10% perp premium would imply a massive 36.5% funding rate paid by longs to shorts. The average transaction costs for the most liquid US equities, which are more efficient than any crypto market, are estimated at around 0.1%. This is consistent with Gemini tic data that show a 0.15% standard deviation in the price change from one trade to the next (reflecting a bid-ask bounce).

The perp premium incenting trades at any instant is below the transaction cost, given not just the fees but gas and the effective bid-ask spread, which is paid twice over a round trip. If one were frequently trading, as the price-setting arbitrageurs tend to do, extreme funding rates would be less than a round-trip in transaction costs. For example, a 50% funding rate would imply a 0.006% funding payment for a one-hour position, considerably less than their transaction costs.

Additionally, the perp premium applied to longs and shorts is based on the average perp premium in the future. Even if one could know exactly one’s perp premium at the time of trade and transaction costs were zero, it would tell the long-term traders little about what it would be in the future. If one targets positions held for a month, the current perp premium at the trade time is irrelevant.

Supposedly, with all the perp premium’s economic insignificance for motivating short- and long-term traders, we expect the market to determine the funding rate by inspiring people to buy and sell perps based on current perp/spot premium movements of 0.02%. This is why it is a farce; it is absurd.

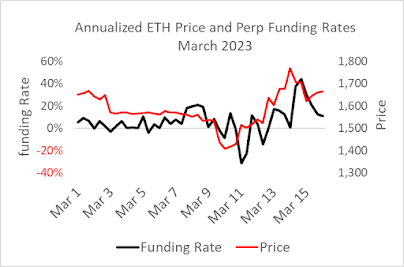

This leads to why the perp premium is consistently positive (payments from longs to shorts) and frequently rises to 40% after crypto prices jump, as it did this week. Market makers dominate price setting, and all perp markets are effectively centralized and run by unidentified and unaccountable coalitions of insiders. They can target 0.03% or 0.13% above the current spot index. No independent auditors regulate an immutable tape of trades with objective time stamps (as the once-perceived compliance-oriented FTX demonstrated). Anything that can be gamed will be gamed, and perp markets can be gamed.

On average, market makers on standard CLOBs have net zero positions on their assets. On perp exchanges, however, the market makers are generally short because it is much easier for these insiders to hedge their short exchange positions with long positions off the exchange [exchanges have different options depending on the nature and size of other markets on their exchanges, so exceptions exist]. A short hedge would require large amounts of capital on another exchange, generating significant operational risk from regulatory attack surfaces and hackers. This allows the perp market makers a significant extra return on the capital needed for market making.

Theoretically, the perp funding rate should be insignificant, if not zero. Neither USDC nor ETH has a dividend on the blockchain. The cost of carry for USDC and ETH are identical. ETH may have an interest rate if one considers the benefits of staking, but this rate is stable and around 4%, implying a negative funding rate (i.e., longs would get paid to compensate for forgone interest). There are no supply shocks in tokens to generate option value, such as when oil tankers are full. There is nothing like a draught destroying a corn harvest that generates a convenience yield for those with corn inventories. To the extent there is hedging pressure generated by natural long or short ETH, the only natural positions are stakers and miners who are perforce long, implying a negative funding rate (they would pay traders to take their naturally long risk).

Nothing in the theory of futures basis rates or funding rates implies the large and variable funding rates we observe in perp markets. Standard efficient markets theory, the law of iterated expectations, implies current sentiment is reflected in spot prices, not forward curves. This is why funding rates are generally independent of asset prices, as with equity swap markets or auto loans.

To the extent there is a correlation between the basis and price movements on standard exchanges, it is unlike the perp markets. In crypto, perp funding rates are generally high when the price has risen, as they did this week, but generally do not go much below zero when the price has declined. This is the opposite of what occurs in commodity markets, where jumps in oil prices correspond to negative funding rates, and big declines correspond to positive funding rates.

Crypto perp funding rates are best explained by insider manipulation. When prices generate windfall profits to long perp traders, they do not mind 50% annualized funding rates the following day, which amounts to a mere 0.14% daily charge. It’s like how big winners in Vegas often give the dealer a big tip: house money. The 50% funding rate premium on perps relative to the regulated and more transparent CME in February 2021 reflects insiders taking what they can from abused customers. Market makers, generally short, receive the funding rate windfall; the game is rigged as heads-they-win big, tails-they-win-a-little.

The theory that explains the positive return/funding-rate correlation is a typical story that is clear, simple, and wrong. It makes no sense when you get into the details. Like the explanation that price increases come from 'more buyers than sellers,' the idea that long demand shows up in futures price premiums has never made sense.

The perp funding rate reflects insider manipulation of customers, a crypto-crypto cost that, if eliminated, would create a superior exchange for those wanting leverage. Some of these exchanges are under quasi-regulatory control, which would be a good issue for regulators to rectify, as it is indefensible, and there is a lot of data out there.

No comments:

Post a Comment